Markets in a Minute - Déjà Vu: Low-Quality Stocks Are Rallying Again, but Time Isn’t on Their Side

Does quality still matter when it comes to stock picking? After a remarkable run for certain low-quality stocks, i.e. those without reliable corporate earnings or strong balance sheets, investors could be forgiven for wondering whether it still pays to focus on the fundamentals.

In this week’s Markets in Minute, we explore what’s driving the tremendous performance of these low-quality companies and why the answer to the question above is (as always) a resounding “yes.” Below, our friends and partners at L2 Asset Management focus on small-capitalization stocks — where the outperformance of low-quality stocks has been particularly stark.

The Original Meme-Stock Craze

The pandemic may seem like a distant memory, but it actually set the stage for trends that are driving today’s outperformance of low-quality stocks.

Flush with government-stimulus cash and free time, individual (or retail) investors piled into stocks during the pandemic, eager to take advantage of rising equity prices buoyed by historically low interest rates. The widespread adoption of online brokerage accounts also made it easier for households to buy stocks (many for the first time) with a few clicks.

Investing in stocks can be a powerful way to build wealth over time, if it’s done thoughtfully. The pandemic-era rally created enormous opportunity, but it also fueled a wave of speculation among retail investors, most notably the meme stock craze that sent the share prices of a handful of long-struggling companies soaring. When prices inevitably crashed, the craze became a poster child for the pitfalls of chasing what’s popular without regard for company fundamentals and long-term prospects.

Take Two

With low-quality stocks rallying, today’s market shares many similarities with the meme-stock rally of late 2020/early 2021. Over the past year, retail investors have once again rushed into stocks with astonishing speed, emboldened by falling interest rates and the artificial intelligence (AI) boom.

These investors’ appetite for stocks has been especially strong since the tariff-induced selloff in early April. After the so-called tariff tantrum, the Federal Reserve faced enormous pressure to resume its rate-cutting cycle and, in fact, has since cut its benchmark rate to the lowest level in three years amid a weakening job market. In July alone, retail investors bought more than $10 billion in equities, reversing a yearlong selling trend, according to S&P Global Market Intelligence.

Why Worry?

As during the pandemic, it appears that many retail investors aren’t buying based on company fundamentals, but instead jumping on the proverbial bandwagon, particularly when it comes to stocks tied to the AI boom.

Since the start of September, the Citigroup Retail Favorites Index, a basket of stocks most favored by nonprofessional investors, has risen a whopping 30%, dwarfing the modest 6% gain for the S&P 500 index. What’s more, some AI-related stocks have risen by 40% in a single day on mere partnership announcements. We’ve even seen a reboot of the meme-stock craze that grabbed headlines during the pandemic.

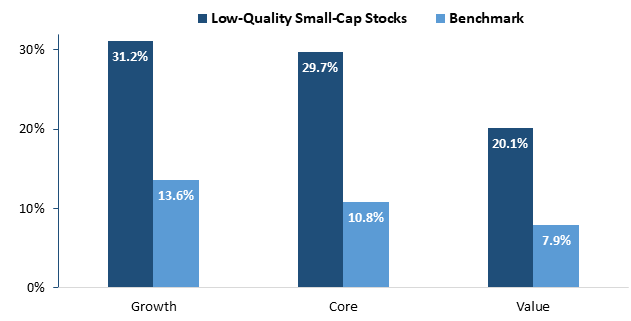

Speculation and momentum chasing have led to wide performance gaps between high- and low-quality stocks, particularly in the small-cap world. Across growth, core, and value stocks, the lowest-quality names — those in the bottom 20% of their benchmarks based on return on equity (ROE) — have outperformed significantly. (Return on equity is one of the best ways to gauge how profitable a firm is relative to the amount of equity capital invested in it.)

Low-Quality Small-Cap Stocks Have Outperformed their Benchmarks Over the Last 12 Months

Benchmark represented by the Russell 2000 index. Low Quality Small-Cap Stocks are represented by stocks in the bottom 20% of their benchmarks based on return on equity. Source: L2 Asset Management; Data from 9/30/2024 – 9/30/2025

History Lessons

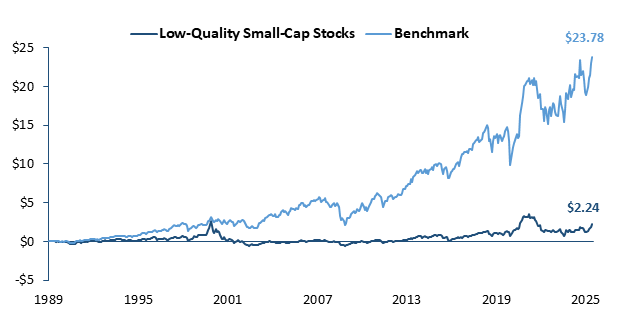

As tempting as it may be to ignore fundamentals when the market is reaching new highs daily, history shows that rallies in low-quality stocks usually have a short shelf life. Over the past 30-plus years, low-quality, small-cap stocks have notably underperformed their benchmarks.

Even a small difference in returns that repeats year after year can become a significant difference in the growth of an investor’s portfolio. Since 1989, low-quality, small-cap stocks have underperformed the total return for the Russell 2000 Index substantially. While the Russell 2000 delivered a compound return of more than 2,000%, low-quality stocks barely grew, often treading water through multiple cycles.

Growth of a Dollar: Low-Quality, Small-Cap Stocks versus Benchmark

Benchmark represented by the Russell 2000 index. Low Quality Small-Cap Stocks are represented by stocks in the bottom 20% of their benchmarks based on return on equity. Source: L2 Asset Management; Data from 4/30/1989 – 9/30/2025

The Takeaway

Chasing stocks with soaring share prices may be tempting, but, as the data show, if those share prices are not backed by strong fundamentals, they are typically not a path to enduring wealth. We encourage investors to ignore the noise and focus on high-quality companies who have strong earnings.

Matt and Sanjeev

“Successful investing demands patience and persistence. Minimize downside risk, buy mispriced cash flows and reduce costs.”

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.