Markets in a Minute - From Wall Street to Main Street: Why M&A Matters for Everyone

Mergers and acquisitions (M&A) are more than headline-grabbing stories about big companies joining forces. They’re a powerful engine behind market momentum—reshaping industries, creating opportunities for investors, and offering business owners a way to grow or exit.

M&A activity can also give us an important read on economic momentum. Strong activity often signals confidence in the economy. Companies are willing to spend, take risks, and bet on future growth. A slowdown usually reflects caution—tighter credit, economic uncertainty, or a wait-and-see mindset. What is M&A activity telling us about the broader economy?

A Big Driver of Market Confidence

At its best, M&A is a shortcut to growth. Companies use acquisitions to expand quickly, enter new markets, or bring in talent and technology they can’t build in-house. That’s why active deal-making is often seen as a sign of optimism. In 2021, for example, global M&A surged past a record $5.6 trillion amid cheap financing and high CEO confidence, reshaping sectors from tech to healthcare. In the same year, the S&P 500 recorded a 29% return.

From Boom to Slowdown to Rebound

But the record-setting pace of 2021 wasn’t built to last. As interest rates rose and inflation took hold, the momentum faded. From there, the pendulum swung back towards caution for the next two years. By 2023, deal values had slipped by 45% to around $3.1 trillion.

In 2024, deal activity rebounded 12% year-over-year to $3.4 trillion. However, compared to the size of the global economy, M&A remained unusually subdued, with deal value as a share of GDP near 30-year lows.

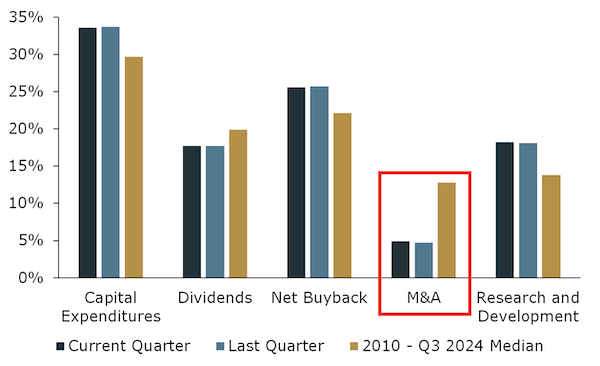

While higher financing costs, which make acquisitions more expensive, was the primary driver for muted M&A activity, AI-related capital expenditures and research and development pulled corporate cash toward building new infrastructure rather than buying companies.

S&P 500 Quarterly Cash Use Percentage Breakdown

Past performance is not a reliable indicator of current or future results. Source: Kestra Investment Management with data from 22V Research.

2025: Optimism With a Twist

This year began with cautious optimism. Transformations in technology created urgency for companies to strengthen their AI capabilities, tackle infrastructure challenges tied to soaring power demand, and prepare for the next phase of growth.

In the first half of 2025, deal values jumped 29%, driven by eye-catching mega-deals like the acquisition of US Steel and Walgreens, both worth over $10 billion each. Global dealmaking reached $2.6t, the highest for the first seven months of the year since 2021, despite economic and geopolitical uncertainty. While the overall value of M&A transactions suggests robust activity, the overall number of transactions declined compared to the same period in 2024.

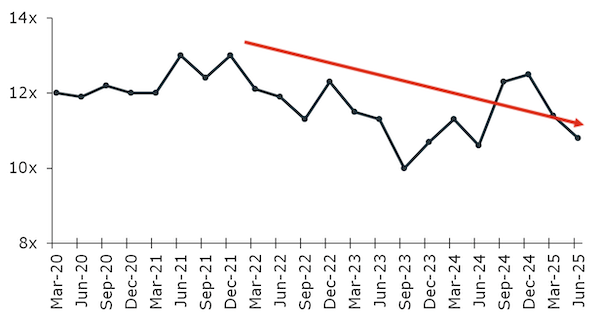

The typical price paid for companies, represented by the enterprise value / EBITDA (earnings before interest, tax, depreciation, and amortization) multiple, is also up slightly year over year, but about 17% below the peak seen in 2021.

Median Multiple Paid by Acquiring Companies (EV / EBITDA)

Past performance is not a reliable indicator of current or future results. Source: Kestra Investment Management with data from PwC.

The Road Ahead

Over the next year, investors expect M&A to slowly gain momentum, helped by easing inflation and the expectation of lower interest rates, which could reduce borrowing costs. Additionally, policy shifts, such as tax cuts and deregulation, are helping unlock stalled deal activity.

Massive investment in AI infrastructure - including data centers, power, and network capacity - is poised to be a major M&A driver going into 2026 as companies compete to secure the physical and digital platforms that power generative AI.

Why Small Business Owners Should Pay Attention

While mega-deals attract the most headlines, small and mid-sized businesses account for most deals by volume. In 2024, 95% of all transactions were under $1 billion, and for the first time in four years, the number of these smaller deals actually grew. Much of this was driven by retiring baby boomer owners and new buyers, with nearly 38% of small business sales in 2024 due to owner retirement.

For sellers, demand is steady, but financing is a hurdle. Despite the Federal Reserve lowering rates in 2024, banks remain tight with credit. 91% of business brokers say seller financing will be critical for closing deals in 2025.

The Takeaway

2025 may not match the frenzy of 2021, but there are signs that companies are once again beginning to look outward, using acquisitions as a tool to reinvent and grow. That means M&A will continue to shape not only Wall Street headlines, but also opportunities on Main Street.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.